(Disregard this if it's keeping you awake at night and looking at planning scenarios during the day.)

It's taken me a couple of weeks to process it, but here's a new model of climate change costs in a recent Nature article The economic commitment of climate change. From the abstract (emphasis mine):

Global projections of macroeconomic climate-change damages typically consider impacts from average annual and national temperatures over long time horizons. Here we use recent empirical findings from more than 1,600 regions worldwide over the past 40 years to project sub-national damages from temperature and precipitation, including daily variability and extremes. Using an empirical approach that provides a robust lower bound on the persistence of impacts on economic growth, we find that the world economy is committed to an income reduction of 19% within the next 26 years independent of future emission choices (relative to a baseline without climate impacts, likely range of 11–29% accounting for physical climate and empirical uncertainty).

Those are huge losses already baked-in: if anything, our current emission path and actual investment are moving in the opposite direction, meaning that we are looking forward to a generation of income headwinds of more than 1% a year in income growth every single year - and after that it gets bad.

From the blog post linked above:

The key part: Oil and gas companies investments are incompatible with a level of fossil fuel usage that keeps global temperatures beyond catastrophic thresholds. “Incompatible” as in “double what they should be, and not looking like that’s changing any time soon.”

I'm aware, and so are the authors of the paper, of the difficulties of this sort of forecasting. But saying that something is hard to forecast isn't the same as saying that a careful forecast is worth as much or as little as an (un)informed guess. This model adds some new information and a new approach to the issue. At the very least, it should move your expectations down.

In any case, that 19% of lost income against the baseline is the global projection. As you can imagine, the scale of damage to the poorer countries is much larger at the same time that their ability to pay for even basic harm-reduction measures is much smaller (see e.g. this note from the notorious communist snowflakes at the IMF). Even if you ignore the horrendous human losses involved (and it'd be worrying if you can do that), pretty much the entirety of history for at least the last couple of centuries shows that there's no such thing as a "local" problem.

There are also paths of harm to the developed world that are quite direct — they are already causing damage — and extremely legible to the financial system. For example, here's a starkly humorous story of California firefighters unable to maintain the infrastructure they need to deal with sharply increased fires because they finance it through bonds based on the value of their properties... which need to be insured... which insurance companies decline to cover... because of the sharply increased fire risks.

Insurance here works as an early reaction system, but the basic financial story is simpler: much wealth is based on property values, much of property value is sensitive to how often it gets burned down, flooded, hit by tornados, rendered nearly unlivable by a heat wave, etc., and all of those factors are getting steadily worse. Which means that there's a large component of generally productive assets (including livable cities) in the world economy that are scheduled to get hit, with huge first- and second-order impacts. The next Dust Bowl isn't going to be kind to the stock market, if that's your main concern.

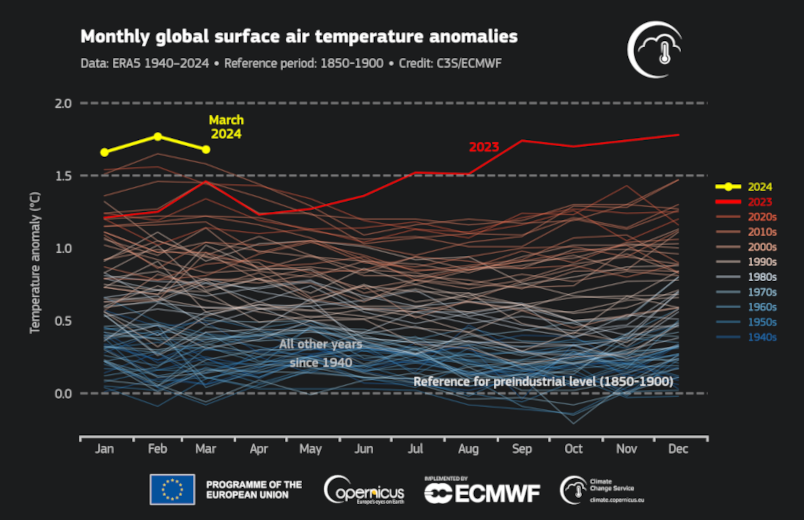

To emphasize the fact that this is all moving faster than even climatologists expected, here's a graph from the helpfully titled article Copernicus: March 2024 is the tenth month in a row to be the hottest on record from the EU's Climate Change Service:

None

Back to the fact that we are going in the wrong direction to keep damages down to that already terrible baked-in level, the well-known ecofanatic Larry Summers co-wrote with N. K. Singh an op-ed titled The World Is Still on Fire. A fragment:

Despite the bold rhetoric, 2023 was a disaster in terms of support for the developing world. As the chart below demonstrates, rising interest rates and bond and loan repayments meant that nearly $200 billion flowed out of developing countries to private creditors in 2023, completely dwarfing the increased financing from the international financial institutions. “Billions to trillions,” the catchphrase for the World Bank’s plan to mobilize private-sector money for development, has become “millions in, billions out.”

They add later in the article:

Setting aside the complex problem of climate change for a moment, world leaders haven’t even been able to tackle the simplest, most straightforward challenges. War, inflation, and poor governance have brought some of the poorest people – including in Chad, Haiti, Sudan, and Gaza – to the brink of famine, yet the international response has been slow and muted. This is both a humanitarian disaster in its own right and a symbol of our broader inability to act in the face of a crisis.

Their suggestions, though, are very much "let's try somewhat harder." The closest they get to acknowledging that this isn't enough is

Second, transform MDBs [multilateral development banks] into big, risk-taking, climate-focused institutions. Development banks have tinkered around the edges with bolder approaches to lending, but it is time for them to scale up those efforts. The wealthy countries that are the biggest shareholders in the multilateral system need to provide the political support for that risk-taking.

That's an understatement. Vaclav Smil, one of the world's foremost experts on large-scale technology systems, claims that in fact net zero is too big an undertaking to fully realize in any sufficiently short timeline even if we start moving in the right direction and as fast as we can. This isn't, note, "going for net zero as fast as we can is worthless." Not going for net zero as fast as we can is catastrophic. The best we can achieve isn't great, but it's much better than the worst that can happen.

One good news — or rather a positive development that's no longer news — is that the marginal cost of renewable energy generation has fallen so much that it's no longer the main problem. The bottleneck now is in the raw materials and money for transmission and storage (and, absurdly but true enough, permits and regulations; some say the world will end in fire, some say in ice — it might well end in infrastructure vetoes designed to maintain local property values and own the libs). Perhaps harder is the decommissioning of carbon emitting energy generators and processes. I think Smil is right that we can't do this fully any time soon, but by and large we aren't doing it at all. Climate change damages aren't diminished by adding renewable energy sources and electric transportation. They are diminished by removing carbon emissions; everything else is just a prerequisite to making it feasible.

So, not really good news.

That's where we are. What do we do, not in the sense of what the world should do if we were fully coordinated and aware of this — if we were we wouldn't be here — but rather of what do we do with the level of coordination and resources we have now?

I don't know. I do have some ideas about what's basically certain to happen, and what they means in terms of proactive preparation and active response:

- Disasters are going to happen more frequently, be more damaging, and leave deeper long-term damage. As Summers and Singh note, we are currently quite bad at dealing with them. We should figure out pre-arranged credit lines to finance response at the adequate speed and scale, and similarly have sufficient plans and people on the ready. Resilience is a global feature, not a local one, and you have to build it beforehand.

- Both the energy transition and the damage-handling we'll have to do for the problems we're already facing will be among the largest and most complex projects humanity has ever done. It's unlikely that it can be done with the current set of financial institutions and tools, and I'm certain it can't be done with the current set of project design and management political and technological practice. We need to develop and deploy new ways of conceptualizing and deploying planetary-level financing and hyper-complex project development and governance (an area where I think the potential of AI is under-hyped, for certain types of "AI").

- Authoritarian, anti-science, and isolationist forces — both inter- and intra-national — will grow even more. This isn't a problem specific to climate change, but it can be as forceful an impediment to handling it as any technological or institutional difficulties.

And, of course, we're certain to face at the same time any number of other crises: our political and institutional "operating systems," so to speak, aren't usually built to handle that sort of strategic complexity in a resource-efficient manner.

It's clear that we're past the time when we can make a dent on this issue by raising ecological consciousness, sharing cars, or unplugging laptop chargers. The scale and speed of the problem requires nothing less than a qualitative jump in our scientific, engineering, financial, political, and organizational infrastructures.

If there's a silver lining — and I'm pushing myself hard to find one — it's this: Don't be afraid of learning and working on truly weird and new technologies and processes even if you don't see demand for them right now. Very little of how we do things today is still going to be adequate in twenty years — even more so as other economic, social, and technological shifts hit us from every side — and the need for things that work better, even if they are an unsettling kind of new, is going to be stronger than the universal preference for things that are "new" in familiar ways.

Hunter S. Thompson famously wrote When the going gets weird, the weird turn pro. If everything you're working on makes sense to everybody else right now you're probably behind the curve. It's getting weirder than you think faster than you'd expect and it's not going to stop.