To exploit the quantitative dynamics of investor attention, like any other price-like signal, the first thing to understand is what a signal is and isn't informative about. What, really, can we say about the world based on what people are saying?

A very useful classification distinguishes between secular topics and information shocks.

Secular topics: keeping up with the Kardashian Space Program

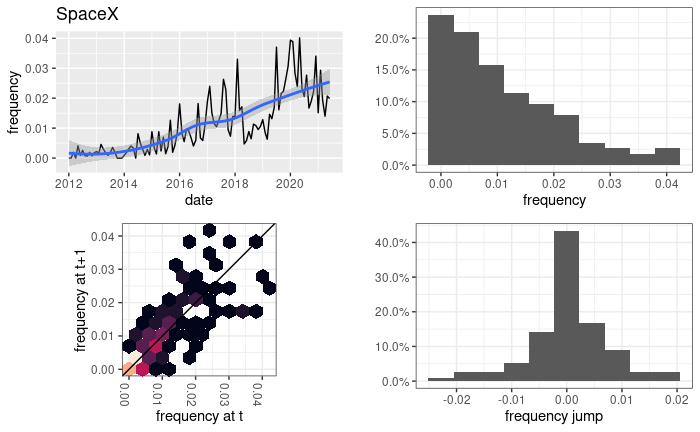

A secular trend is a topic characterized by a possibly biased random walk around a relatively high level of interest. Consider for example SpaceX:

The term frequency timeline — a proxy for how often it's mentioned in the "investment discourse sphere" — is consistently high, but equally interesting are the histograms and transition map. These are typical of a random walk, which in an asset market is consistent with informational efficiency. However, in an informationally efficient process you should see new information as coverage frequency, not as changes to it.

To put it in another way, under parsimonious assumptions about the real world, if the coverage about SpaceX were related to the "size of the surprise" of information newly available about it, there should be much less mid-sized frequency jumps, and more of the frequency mass should be closer to zero; the amount of autocorrelation shown by the transition map is not compatible with a model in which more coverage imply more news (in the information-theoretical sense).

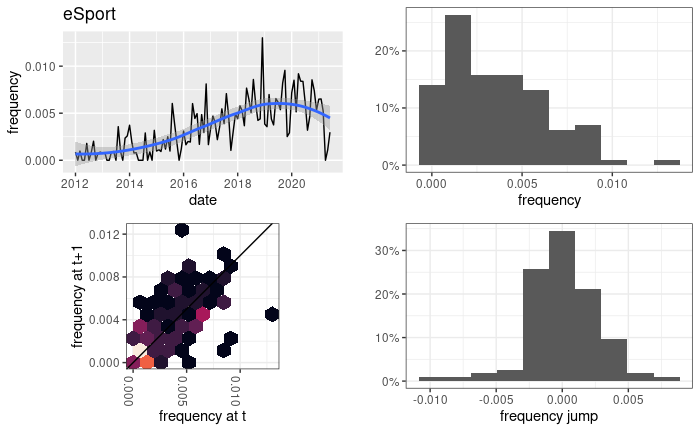

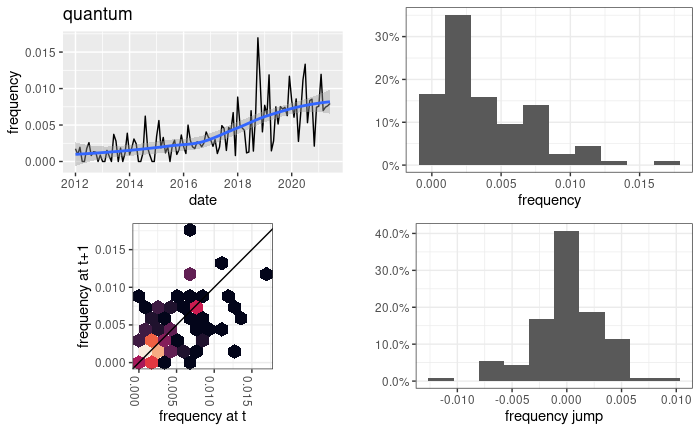

We can see a similar pattern on eSport (and variants) and quantum, with different long-term dynamics but the same statistical pattern:

These are all in essence topics that the market talks about because they have been talking about them. This isn't an analysis of whether there are good or bad reasons to do that; we are just looking at the pattern itself.

Information shocks: it's always the ones you don't expect

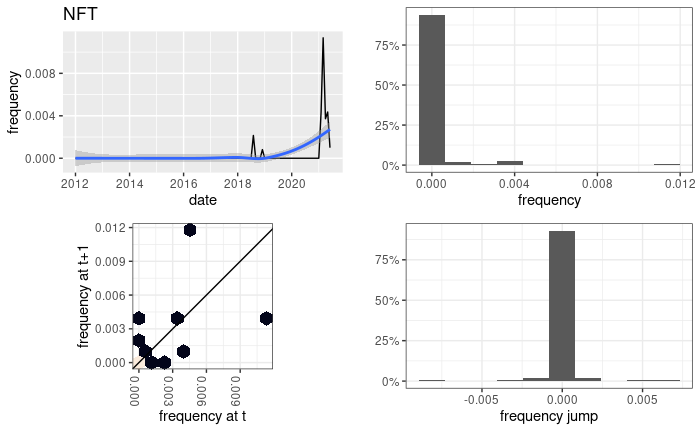

The investment community has its secular topics, its deep dives, its continuous monitoring of the known frontiers... but the shocks come anyway:

It's possible that over time the statistical patterns of NFT will come closer to the previous examples, but right now NFT is a clear information shock: a huge spike in an otherwise flat timeline, corresponding to the ingestion by the market of, well, shocking new information, rather than the gradual increase in interest seen in other topics.

What's interesting about what one might call the microstructure of the tech-oriented investment attention market is that talk about NFTs began most in earnest after mainstream coverage of Beeple's auctions. As a technology, NFTs had been talked about and then pretty much forgotten (there are always millions of exceptions to statements like these; the Investment Climatology Project is about trying to understand approximate trends). It exploded when an external actor achieved unexpected success in an outside environment, reported by equally unexpected media: if one wanted a leg up on the NFT trend, the thing to read turned out to be Esquire.

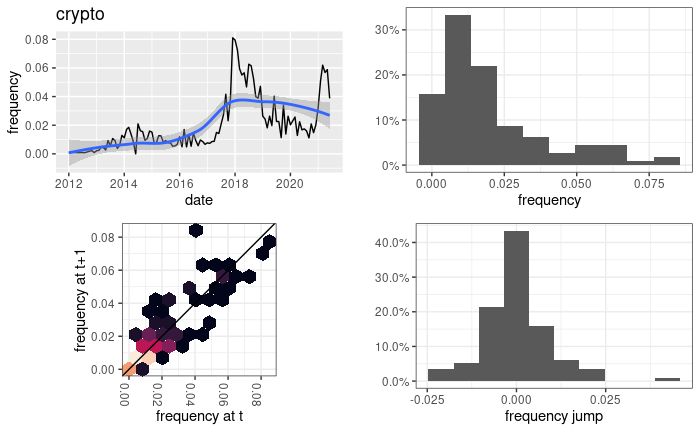

The combination of these archetypes — the secular topic and the informational shock — helps explain the perpetual strangeness of the crypto coverage. It's very much a secular topic, but open to external information shocks (often in the form of huge price changes) in a way than other secular topics aren't:

How to read the information market

The examples above show two aspects of the investment climate content that take a central place in the research of the Investment Climatology Project:

- Coverage frequency isn't information content. How much a topic is talked about is often more a function of the topic itself (of its social standing in the investment community if you will, or of the hopes and effort already put on it) than of whether there's significant new information about it. It's worth re-emphasizing that this is in the information-theoretical sense. You can write entire books every week about anything without exhausting the topic, but you would be refining and adding detail, and only rarely changing its basic relevance.

- Shocks come from the outside. In a way this is a tautology, but as the investment world sometimes describes itself as generating innovation, it's interesting to see that in many cases it's rather an innovation repackager. Not always: SpaceX has been tracked since its birth, and whatever comes out of quantum computing, it won't be a surprise. But the information market is not always good at capturing the development of new phenomena of interest until after it has broken a threshold not always on this side of "mainstream knowledge." The linear model of R&D first, then investors, then the newspapers, is much more bidirectional than often assumed even by them actors themselves.

As sociologically interesting as these phenomena are, from the point of view of the practical exploitation of quantitative dynamical patterns they offer clear opportunities, and they align with two of the long-term goals of the Project:

- Compensating for statistically sub-optimal patterns in attention markets to make them more useful as sources of information about the world.

- Leveraging statistically sub-optimal patterns in attention markets to make them more useful as sources of information about the actors in them.

(Spanish article at Instituto Baikal)

None

None

None

None

None